Welcome to Euronomics, every week there will be an update of European economic related news. In this edition I will discuss wether or not Japen could be a good economical parter for the EU.

Last 6 weeks, I’ve been searching for information about economics of EU and Japan for the economic class. Sometimes I did in English but basically in Japanese. In other words, I looked on it from the view point of Japan. Looking at the Internet, I found that there is much less information regarding EU compare to the United States or Asian countries. In this article, I’d like to think over the economic relationship between EU and Japan.

If you see the number of articles on the Internet, it’s obvious that there’s less interests and attention on EU as for economic. Below you can see the numbers of article of each search words.

‘韓国 日本 経済(South Korea Japan economic)’ 20.100.000

‘中国 日本 経済(China Japan economic)’ 16.200.000

‘アメリカ 日本 経済(the US Japan economic)’ 13.800.000

‘EU 日本 経済(EU Japan economic)’ 2.810.000

‘オランダ 日本 経済(the NL Japan economic)’ 498.000

Also, personally I thought the economic relation was weak between EU and Japan. As an Exchange Student, I’ve lived in the Netherlands for 7 months and found that there are only few products from Japan I can buy. There is one Asian grocery store in my city but most of products there are from China and South Korea. Even if I can find one, it is incredibly expensive. For instance, you can buy Mattcha (Traditional Japanese Green tea) Kitkat for less than 2 euros in Japan. If you want to buy it in the Netherlands, you have to pay 6 euros for the same thing and can find it only in few shops which sell Asian products.

I’ve lived in the Netherlands and travelled around 10 EU countries in last 7 months. And I felt that even it is said the world is globalizing, there are still lots of things we can import/export to share between EU and Japan. I’m sure that it will help us to share our cultures and understand each other. Now EU has weaker relationship for Japan compare to the US or Asian countries though, it can be considered that EU and Japan have a great possibility of growth in economic.

Welcome to Euronomics, every week there will be an update of European economic related news. In this edition I will discuss the difficult current situation in the EU; caused by the many crises on different levels, including the financial crisis.

The European Union has always seemed to be a very stable and integrated union. Coexisting has been replaced by cooperation between the EU countries. This process started in 1951 with the European Coal and Steel Community, consisting of Germany, France, the Netherlands, Belgium, Italy and Luxembourg. This community was built on common values and a common identity. Over the years more countries joined in and thanks to the Cold War Europe had a common enemy. This allowed them to continue building integration and democracy. However, after the fall of the Berlin Wall and the Soviet Union, Europe no longer had a common foe and identity. The only thing keeping Europe together was the economic policy.

The East Bloc countries were soon involved in the transformation of the economic policy. Europe turned from a trade bloc into a financial bloc and saw huge economic growth. In 1994 the Maastricht Treatywas signed which led to the implementation of a single currency called the Euro. All seemed to be going well until the 2008 financial crisis. Once again, Europe is divided. But this time it has nothing to do with enemies from the outside; the threats come from within Europe.

The financial crisis has divided the EU countries into creditors and debtors who cannot agree on how to manage the consequences of the crisis. This means that Europe’s leaders failed to come up with a good solution and instead had to resource in emergency measures which I believe have proved to be unsuccessful.

The financial crisis turned out to be not the only crisis that is dividing Europe. The current migration crisis has contributed as well. On one hand there are countries opening their borders for the refugees (Germany, Sweden), and on the other hand there are countries closing their borders (Poland, Hungary). Besides, there is also a political crisis going on which might even be more severe. There is a growing lack of confidence in the rulers of the EU. Many people feel that the EU should be more democratic; trust in the institutions has decreased significantly over the last few years. This phenomenon is especially visible in the countries that had to deal with austerity measures and sanctions such as Greece and Ireland.

The fact that many Europeans are not satisfied with the EU anymore has a lot to do with the consequences of the Euro zone crisis they encountered. Unemployment rates have been historically low in several countries. Personally, I think that many Europeans are unsatisfied, because they feel like they have no influence on the decisions made by the leaders. A lot of people do not really understand what is going on and what certain measures mean to them. I have often noticed that my friends and family have no idea why it is important that for example Greece and Great Britain stay within the EU. To them, the EU is not democratic and as important as it should be. It is only since I started studying European Studies that I realised the importance and the extent of the EU.

All these different problems are a great threat to the EU integration. As ECB president Mario Draghi said in 2014: “a policy mix that combines monetary, fiscal and structural measures at the union level and at the national level” is what is necessary to achieve economic growth again. I do believe that it is going to be difficult to achieve this. In many countries the people are not very supportive of giving more power to leaders they do not know and did not elect. I would love to know how you feel about this matter, please leave your opinion in the comments!

You can read more about how Europe should be saved here and about how Europe should strengthen integration here.

Figure 1:EU budget or Eurozone budget: Britain’s bluster serves the eurozone well Financial Times 26-11-12

The Eurozone budget has been a topic of discussion for the last few years. Some think a move towards an integrated budgetary framework for the Eurozone would have a beneficial impact on the Single currency and the EMU, others have more concerns. Therefore in this blog I will explain why the EU would need a Eurozone budget, the benefits and drawbacks and how the idea for a Eurozone budget has been brought to live.

The idea for a Eurozone budget was highlighted by the then European Council President Herman van Rompuy. The budget for the Eurozone is currently still part of the EU-wide budget, which is an amount of approximately 130 billion euro’s a year (1% of the EU’s GDP); most of the money from this budget is spend in the areas of agriculture, science, Infrastructure, etc.

Why can the Eurozone just use the money from that EU budget, why do they need their own budget? There are several reasons why a Eurozone budget is necessary. The EU budget is simply too small to provide fiscal stabilization, besides that the budget is also not flexible enough. The only tool the EU now has to fight asymmetric shocks are the national fiscal policies. Economic shocks lead to higher deficits of the national budget, and higher interest rates on public debt; this could pose a serious problem for some Eurozone member states. “Aim of the proposed Eurozone budget is to partly decrease a burden borne by the member states when encountering a negative asymmetric shock and provide temporary transfers to help country decrease impact of the shock on national budgets” (Lukáš Kadidlo, 2015)

What benefits would a Eurozone budget have for the European Union, especially the EMU?

The EU is missing a stabilization function on EU level. In the Eurozone crisis the Eurozone was not prepared to help member states adjust to asymmetric shocks in the early stages of the crisis. The reason why the Eurozone needs fiscal capacity is because the crisis has shown us that not every member state is able to run successful stabilization functions. A permanent insurance mechanism at supranational level need to be established to address the unemployment problem of the southern EU countries.

Secondly, the EU budget is not a federal budget. A common fiscal capacity is a standard feature of other monetary unions, so why is this not the case for the European Union? All other federations have a larger amount of spending than the European Union like in the United States, while in the EU only 2% of public spending is given on a supranational level. The EU budget is planned 7 years in advance and therefore nowhere near flexible enough to perform a stabilization function, you cannot estimate an asymmetric shock in advance; therefore the EU budget cannot provide stability in times of economic crises.

Not to mention, the EU does not even have a central fiscal authority, so they basically do not have a Eurozone Ministry of Finance. A central authority is necessary for bringing in taxes and is able to use financial resources for the entire European Union. This would certainly be beneficial for the stabilization function.

However there are certainly some concerns regarding the establishment of a Eurozone Budget. Several arguments can be given against a Eurozone budget. For example why can the stabilization not be included in the current EU budget, why is a separate budget needed? Instead of establishing an entirely new budget, making some adjustments to the current EU budget would certainly be easier and quicker.

The idea of fiscal capacity within the Eurozone would lead to more federalism in fiscal and political integration; some member states see this as a controversial idea. They do not want to pay more money to the Pan-European level that they already have to with the EU-wide budget.

It would also mean that if a Eurozone budget would be created, non-Eurozone countries will have concerns on the effect it would have on the amount of money available to them. Non-eurozone countries benefit from the EU-wide budget, but a Eurozone budget would mostly be beneficial for countries that are part of the Eurozone.

A eurozone budget will be beneficial for the monetary union, so that they can execute their stabilization function that is so important for the European Union, especially in times of crises, like the recent Eurozone crisis. The EU was not able to use their own financial resources to give financial aid to countries in need; the money had to come from other national governments. However, a eurozone budget, will turn the European Union in a more federalist union, the question therefore is we willing to give the EU more authority over fiscal policies of national governments?

Welcome to Euronomics, every week there will be an update of European economic related news. In this edition a difference between the FTA and EPA will be explained.

Nowadays, there are lots of economic partnerships because of the progress of globalization. In this blog, I would like to explain a difference between FTA and EPA, current situation about FTA in the EU.

FTA: Free Trade Agreement

FTA is an agreement which enables to trade things and services freely by eliminating regulation to specific organizations and abolish tariffs between some certain countries.

EPA: Economic Partnership Agreement

EPA is an agreement which aims to tighten up relationship between countries and areas by cooperating in various fields such as not only logistics but also free movement of persons, protection of intellectual property rights, investment, competitive policy and so on.

Lots of FTA has been concluded every year. According to the Jetro, 266 of FTA are already put into effect and 120 of FTA are under negotiation today.

In the EU, there are seven FTA such as Stabilisation and Association Agreement, Association Agreement, Free Trade Agreement, Deep and Comprehensive Free Trade Agreement, Economic Partnership, Interim Economic Partnership Agreement and Customs Union. The EU Commission published “Global Europe: competing in the world” on October 4 in 2006. At the point, the commission has turned negative attitude towards FTA into positive. As a result of this, negotiation for FTA between EU and Asian countries has been going actively. To survive the competitive global market, we should keep eyes on the changing economic situation.

Welcome to Euronomics, every week there will be an update of European economic related news. In this edition the BBC Documentary The Great Euro Crisis will be discussed.

Greece has been in a very big crisis for years now, but can this be blamed on the Euro or not? Has this crisis united the Euro zone or pulled it apart? That is the question that is asked in the BBC documentary The Great Euro Crisis. According to the British and eurosceptic presenter Michael Portillo the Euro is the definite cause of Greece’s problems.

When Greece joined the Euro it became uncompetitive and the people started to import luxury goods excessively, since the Euro made import from countries as Germany less expensive. Besides, the availability of cheap credit made is easier to finance luxury purchases. Greece has profited as well from new infrastructures and modern technologies. However, these couldn’t be manufactured in Greece and therefore had to be imported with borrowed money.

According to the Greek people, the Euro is not the cause of the crisis, it is the politicians’ fault. The corrupt political system, the weak institutions without a fair tax system and the lack of investigating cheaper alternatives for projects such as the 2004 Olympic Games, have contributed to the distrust of the people towards the politicians. They still have faith in the Euro for the future: “It is not the Euro’s fault if the government made the wrong choices.”

All the persons interviewed in the documentary believe that the Euro has been good for Greece and Europe in general and that Greece should definitely not leave the Euro zone, since that would only be a step backwards. I tend to agree with these people, however I believe that Greece will not be able to recover from the crisis, if the austerity measures remain this strict and just become more and more. Greece has reached a limit and at this point the people are really starting to suffer. Somehow the EU has to come up with a solution to this very complicated problem that will not destroy the country and its people.

Even though this documentary has been made 4 years ago, the troubles still haven’t disappeared yet. 2016 is to be very unpredictable and the hardest part is yet to come. Prime Minister Alexis Tsipras believes the end to the crisis is in view, but the people find it hard to believe. Read more about the current situation here.

You can watch the documentary below:

What do you think of the crisis in Greece and how should it be solved? Leave your opinion in the comment section!

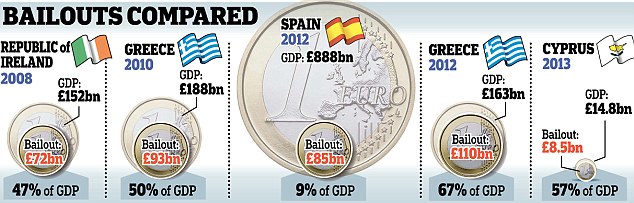

Welcome to Euronomics, every week there will be an update of European economic related news. A few weeks ago we already discussed the exit of Cyprus from the EU bailout program. This blog is a follow-up of the previous blog about Cyprus, in which we go more into depth about the austerity measures and the actions taken by Cyprus resulting in their leave from the European Bailout Program, and would the Cyprus example also work for Greece?

A visual description comparing the different countries within the European Bailout program and its relation to the GDP ; source: Dailymail

As we discussed a few weeks ago, Cyprus managed to climb out of the European Bailout Program very successfully, resulting in economic growth with money to spare. In comparison to other countries like Spain, Ireland & Portugal, Cyprus certainly did a better job in restoring the economy and therefore received a lot of appraisal for their success. However the question remains “How did they do it?” what were the exact austerity measures and the implemented reforms that led to Cyprus leaving the European Bailout Program?

First let’s discuss the views on austerity measures in general. Crisis management based on austerity is to restore market confidence in cases of a financial crisis or government debt crisis. The reason behind a crisis is seen as a disappearance of trust in the economy, in order to regain this confidence, crediting should revive, together with an increase in investments. All of this needs to be achieved through a well-balanced fiscal position and appropriate strategies.

The austerity measures for Cyprus mainly focused on changes of the pension system with a reduction of pensions, changes in the public sector with a reduction of funding, a restriction on the availability of certain social benefits and the introduction of a privatization plan. Besides this banking controls were also implemented.

Cyprus already received a package of austerity measures in 2010/11. The first package of austerity measures was an attempt of the government to raise revenue. The measures included amendments to the law and/or taxation. The following amendments were made;

Increase of Defence tax on interest from 10%-15%. This increase had both an effect on Cypriot residents and organizations. Non residents did not fall under this defence tax on interest payments.

Increase of Defence tax on dividends from 15%-17%. This increase is applicable to tax residents of Cyprus receiving dividends, on distribution rules and applies to tax resident companies who do not distribute at least 70% of its after tax profits with 2 years. All these measures do not apply to non resident individuals or corporations.

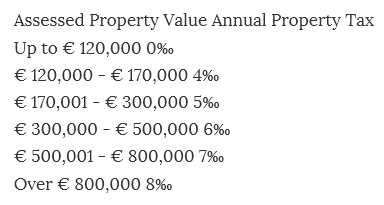

new rates of the Immovable Property Tax , The new rates of immovable property tax, applicable to both individuals and companies owning property within the Republic of Cyprus changed to the following rates from the 1st of January 2012 .

Annual Company Levy: as of 2011 all companies are obliged to pay an annual company levy of 350 Euros. The maximum levy is around 20,000 Euros.

As shown in the four points above you can see that Cyprus raised its taxes and customs in several areas. Besides this they also intervened in the job market. All of these measures were part of the first package of austerity measures imposed on Cyprus in 2012. All the austerity measures from the first package were not enough for Cyprus to get back on track with their economy. Certainly not after the sovereign debt crisis of Greece in 2012. Cyprus was forced to apply for the European Bailout program in June 2012 (discussed in previous blog about Cyprus), bringing them back to the beginning of the financial crisis.

The rescue package of 2013 received from the Troika introduced new austerity measures. The measures mainly focused on the reform of the banking system with the closing of the Laiki Bank. The new measures did not have an impact on deposits below 100,000 Euros. The accounts of Laiki Bank were transferred to the Bank of Cyprus. The bank of Cyprus survived, but did however not receive any money from the bailout program, and above that due to the transfers of Laiki Bank, the Bank of Cyprus also received the 9 billion Euros debt the Laiki Bank had with the ECB. Unlike the other countries from the EU Bailout program, the financing for the banks came largely from the out sized banking sector, namely the depositors above 100,000 Euros, many of these depositors were Russian Businessmen, while other banks in other countries received government funding. On March 16thCyprus’s president, Nicos Anastasiades, desperate to protect Cyprus’s status as an offshore banking model for Russians, had decided to save the two biggest banks and thus to spread the costs evenly. He would have applied a heavy tax to all depositors: 9.9% for those too big to be covered by the EU-mandated €100,000 deposit guarantee, and 6.75% for the smaller depositors. His attempt failed, due to massive withdrawals from deposits from banks, a different decision was made: to apply the pain much more intensely, but on a smaller number of large depositors. The main difference with the other Bailout countries was that Cyprus used deposits from lenders with deposits above 100,000 Euros most of them being Russian businessmen, instead of government money or money from European funds.

Information concerning the other austerity measures and reforms are not mentioned, there is no clear explanation on the exact changes of the pension system and public sector. This does not come as a surprise since the biggest changes happened within the banking sector.

In my opinion, the case of Cyprus is an exception when you look at the other countries from the European Bailout Program. Cyprus introduced controversial reforms and measures no European country has ever used before, the banking sector drastically reformed and financing for banks did not come from the government or the EU, instead the highest deposits had to pay the price. Therefore in my opinion we cannot say Greece will exit the European Bailout Program by using the same measures Cyprus used. We are talking about two different countries with two different economies. In my opinion there is no such thing as an austerity program that works the same for each country. There are certainly similar problems that can be solved by using general reforms and measures, but this will not solve the entire problem. So to conclude my opinion, I think Cyprus was able to find the flaws within their economy, within their banking system, and they acted upon it. They introduced reforms and changes that led them back to a more stable economy. Greece should follow the same example, looking for the real problems that led to their current situation, and act upon it, even when it means that the initial costs for the solution will be significant.

In conclusion, all of these points discussed above show the austerity measures Cyprus imposed from their first attempt in 2010-2011 and their second attempt in 2013 as a result of becoming part of the European Bailout Program, with mainly reforms within the banking system of Cyprus and some other reforms in other areas, Cyprus managed to get back on track, mainly thanks to the reforms of the banking system and the money received from the European Bailout Program.

If you want to read more about the exit of Cyprus from the European Bailout Program and the austerity measures and reforms they used click on the links below.

Welcome to Euronomics, every week there will be an update of European economic related news. In this edition we will discuss the process of signing the EPA between the European Union and Japan.

Diplomatic handshake between countries: flags of European Union and Japan overprinted the two hands

Nowadays, 10% of Japan’s export goes to the EU. This makes the EU Japan’s third largest trading partner. To the EU, Japan is an important trading partner, since it has the second largest trading ration in Asia. Because of these two facts, both countries have been negotiating to establish the EPA (economic partnership agreement). It is assumed that the EU’s GDP will increase by 0.8 per cent and the export figure to Japan will increase 32.7 per cent. As for Japan, this figure will be increased in 23.5 per cent. That sounds like a dreamlike benefit for both. However, can we readily sign off the agreement?

With the EPA, both countries aim to drive down or abolish tariffs and eliminate non-tariff barriers. In more detail, EU and Japan have specific goals respectively.

EU’s prime mark

– Increase the amount of trade regarding staffs and services by driving down the barriers

– Increase the investment flow between EU and Japan by driving down the barriers

– Achieve well-balanced emergence towards each government procurement market

– Abolish tariffs on wines, processed agriculture products

Japan’s prime mark

– Abolish tariffs on cars, parts and electronics field

Some major industry organizations in EU offered their opinion on the FTA. Most of the organizations in the fields of food, agriculture, chemical, medical, electronics and service showed positive attitude. However, ACEA (The European Automobile Manufacturers’ Association) shoot a critical look at it. In Japan as well, there is a negative opinion from agricultural industry organizations especially wine farms since it could negatively affect their economy.

The negotiation between EU and Japan has been carrying forward surely and steadily. There seems to be a positive effect on economy for both. Although, a negative effect also should be taken into account and some measures to protect domestic industries should be put in place at the same time.

Welcome to Euronomics, every week there will be an update of European economic related news. In this edition we take a look at an interesting article published on the World Economic Forum.

So you’ve heard about the Brexit and now you want more information? We found the perfect solution for you! World Economic Forum has posted a blog in collaboration with VoxEU called What impact would Brexit have on the EU? Here you can read all that you need to know.

The subject was briefly touched upon in our post The Monetary Union. On June 23 2016, Great Britain will hold a referendum over leaving the EU. According to the article, the probability that the public will vote for leaving is about 30-40%. It explains what will happen if Britain does leave the EU; what are the political and economic consequences?

This article is definetely worth reading! Please feel free to put your opinions about the article in the comment section below, we would love to discuss this with you.

Welcome to Euronomics, every week there will be an update of European economic related news. In this edition I will explain what the European Commision’s Investment Plan for Europe is.

As explained in the video by the European Commission below, Europe’s economy is only slowly growing after the crisis and investors are still cautious. This is why on November 26 2014 the Commission announced its Investment Plan for Europe. €315 billion is to be invested in Europe over the next 3 years, but what will be done with all this money and where does it come from?

You can find the video and more information by the Commission here.

First of all, the goal of this investment plan is to kick-start long-term investments across various sectors, which were mentioned in the video. The Commission will use already existing funds to stimulate public and private investors. These investors should spent €315 billion in the next 3 years. The plan consists of 3 steps to help achieve the goal:

mobilising increased finance capabilities without increasing public debt

supporting investment in key areas

removing barriers to investment

Launching the European Fund for Strategic Investments (EFSI) was necessary to execute the first step of the investment plan. This fund is a cooperation between the European Commission, European Investment Bank and European Investment Fund. The EFSI focuses on projects that have a higher risk, that will deliver a positive influence on the European economy and in which the EIB has an expertise. It has more than 200 projects in 22 EU countries. To read more about the EFSI you can go to this webpage.

You are probably thinking: “This all sounds very nice, but what does it mean for me?”. Well, that is the problem. The plan says that it aims to create more jobs (more than 1 million in the next 3 years) and to increase economic growth. According to the Commission, the beneficiaries will be small and medium-sized businesses, research and innovation, and infrastructure projects. So unless you own a small business, you probably won’t notice much of this new plan yourself.

Personally, I think that investing in European economy is always a good idea, however the plan does seem a bit optimistic and not as innovative as the Commission says it is. To assume that investors will spend such a big amount of money within 3 years, seems unrealistic, especially from the private investors; people do not have much money to spend anymore. I believe that much more is needed to attract new investors. It requires more than just pumping money into projects; the regulations that concern investing should be revised, to simplify investing.

Welcome to Euronomics, every week there will be an update of European economic related news. In this edition the Japanese interest rate policy will be explained and compared to the European one.

On February 16, for the first time ever, the Bank of Japan adopted negative interest rates with the aim of generating 2% inflation. It is said that Japan’s case will be the most remarkable, since Japan’s economy has been in stagnation for decades, although it is the third largest in the world by nominal GDP. The negative interest rates policy itself was already introduced in Eurozone, Sweden, Denmark and Switzerland. What are the differences between the policy in the EU and Japan? And how will Japan’s policy end up?

In fact, Japan’s negative interest rates policy is operated based on the one in the EU. When it comes to the policy in the EU, the targeted deposits are different. Moreover, its goals were slightly different respectively. The Eurozone and Sweden aimed at price stability while Denmark and Switzerland attempted to stabilize an exchange rate. In Japan’s case, the policy has been adopted for the both of reasons above.

Japan’s main purpose of this policy is to raise the economic growth rate by promoting the financing to organizations or citizens. However, it is questionable if such tactics are effective or not.

In an interview by BBC, Martin Schulz of the Fujitsu Research Institute pointed out the difference of the situation between the EU and Japan. Contrary to the EU, which was forced to introduce the negative interest rates due to the economic crisis, Japan is intending to speed up the economic growth. In addition, he explains the following.

“In Japan, credit didn’t expand not because banks were unwilling to lend but because businesses didn’t see the investment perspective to borrow. Even with negative interest rates, this situation will not change.”

“Businesses don’t need money – they need investment opportunities. And that can only be achieved by structural reforms, not by monetary policy.”

Aside from Mr. Martin, there are some analysts who have doubts about the effectiveness of the policy. There are, however, positive opinions as well. Mr. Kuroda, who is the governor of the Bank of Japan, emphasised that the positive effectiveness of the policy is quite great. He even pointed out that the 2% inflation will likely be reached in 2017 under the present policy.

Since the Lost Two Decades after the Japanese asset price bubble’s collapse in 1991, Japan has been struggling with great stagnation of its economic growth. Although it will take more time to measure the effectiveness, the result of Japan’s negative interest rates policy is attracting attention.